Experts Project Home Prices Will Rise over the Next 5 Years

Even with so much data showing home prices are actually rising in most of the country, there are still a lot of people who worry there will be another price crash in the immediate future. In fact, a recent survey from Fannie Mae shows that 23% of consumers think prices will fall over the next 12 months. That’s nearly one in four people who are dealing with that fear – maybe you’re one of them.

To help ease that concern, here’s what the experts say will happen with home prices not just next year, but over the next five years.

Experts Project Ongoing Appreciation

While seeing a small handful of expert opinions may not be enough to change your mind, hopefully, a larger group of experts will reassure you. Here’s that larger group.

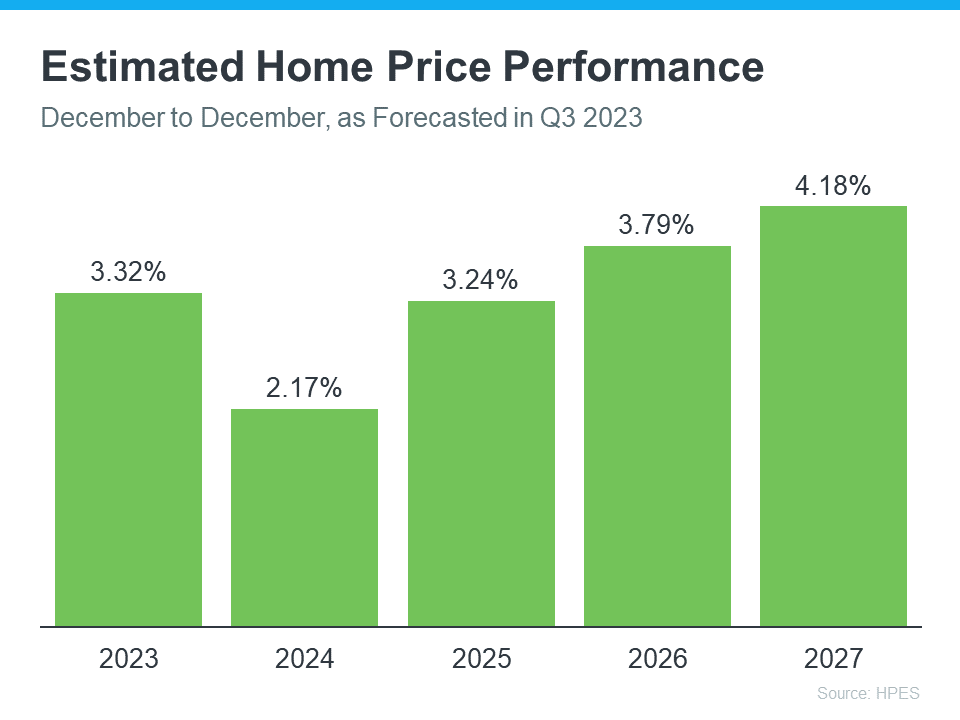

The Home Price Expectation Survey (HPES) from Pulsenomics is a great resource to show what experts forecast for home prices over a five-year period. It includes projections from over 100 economists, investment strategists, and housing market analysts. And the results from the latest quarterly release show home prices are expected to go up every year through 2027 (see graph below):

And while the projected increase in 2024 isn’t as large as 2023, remember home price appreciation is cumulative. In other words, if these experts are correct after your home’s value rises by 3.32% this year, it should go up by another 2.17% next year.

If you’re worried home prices are going to fall, here’s the big takeaway. Even though prices vary by local area, experts project they’ll continue to rise across the country for years to come at a pace that’s more normal for the market.

What Does This Mean for You?

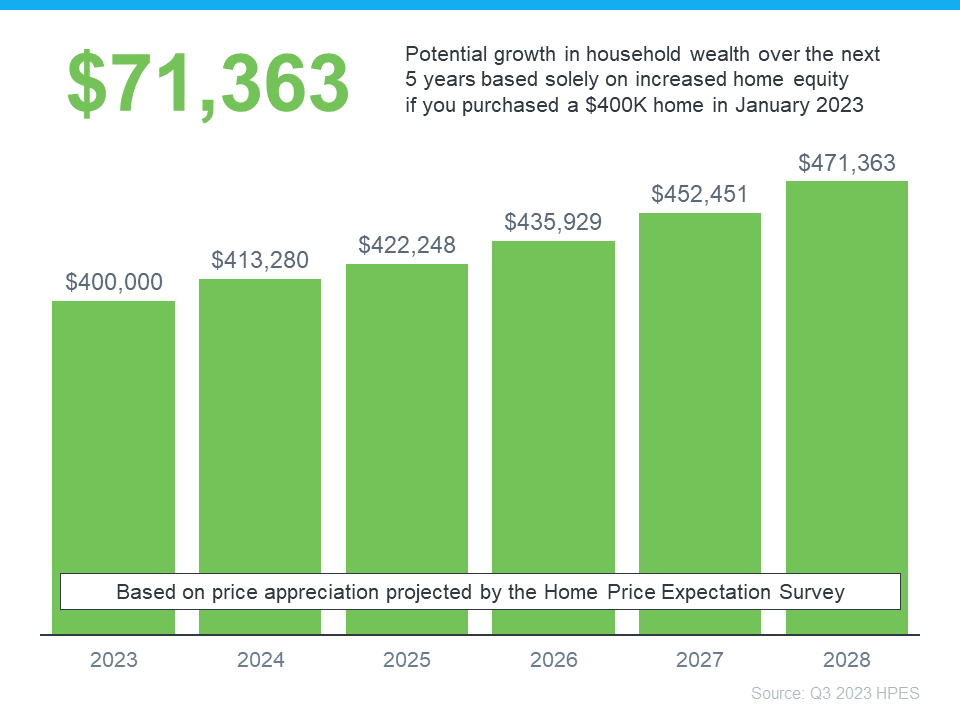

If you’re not convinced yet, maybe these numbers will get your attention. They show how a typical home’s value could change over the next few years using the expert projections from the HPES. Check out the graph below:

In this example, let’s say you bought a $400,000 home at the beginning of this year. If you factor in the forecast from the HPES, you could potentially accumulate more than $71,000 in household wealth over the next five years.

Bottom Line

If you’re someone who’s worried home prices are going to fall, rest assured a lot of experts say it’s just the opposite – nationally, home prices will continue to climb not just next year, but for years to come. If you have any questions or concerns about what’s next for home prices in our local area, let’s connect.

How Buying a Multi-Generational Home Helps with Affordability Today

In today's world of rising housing costs, many buyers are looking for ways to still be able to buy a home. Some of them have found a solution in multi-generational living.

Multi-generational living is when two or more adult generations live together under one roof. This includes siblings, parents, or even grandparents. Here’s an in-depth look at why more buyers are choosing this option today, so you can see if it may be right for you too.

Reasons To Buy a Multi-Generational Home

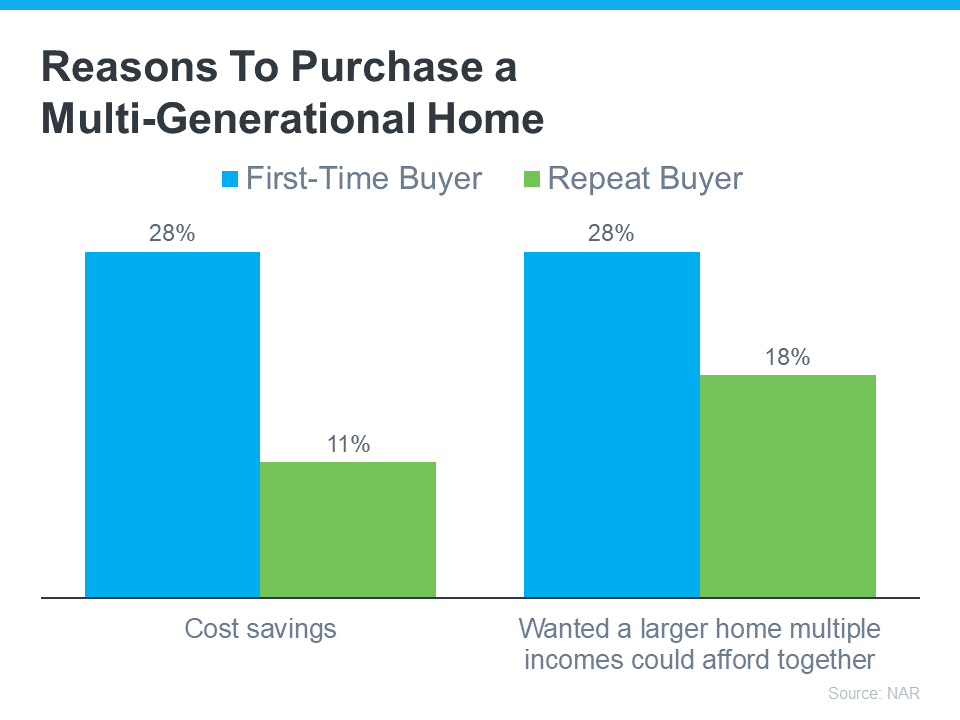

According to a recent study by the National Association of Realtors (NAR), the top two reasons people are opting for multi-generational homes today have to do with affordability (see graph below):

Cost Savings: About 28% of first-time buyers and 11% of repeat buyers are deciding on a multi-generational home to save on costs. By pooling their resources, households can share the financial responsibilities like mortgage payments, utilities, property taxes, and maintenance, to make homeownership more affordable. This is especially helpful for first-time homebuyers who may be finding it tough to afford a home on their own in today's market.

More Space: Another 28% of first-time buyers and 18% of repeat buyers are doing it because they want a larger home they couldn’t afford on their own. For some of the repeat buyers who listed this as a main motivator, it could be because they find themselves taking care of older parents while also welcoming back young adults who've returned to the nest. With everyone chipping in and combining their incomes, suddenly, that big dream home with more space is within reach. As the Triangle Business Journal explains:

“Choosing multi-gen living allows people to purchase a home much larger than they could afford on their own by leveraging the combined income, credit and a down payment of those that they will be occupying the home with.”

Lean on an Expert

If you’re interested in this too, partner with a local real estate agent. Finding the perfect multi-generational home isn't as simple as shopping for a regular house. That’s because there are more people with even more opinions and needs that should be considered.

You've got to make sure everyone has their own space, find room for shared household time, and possibly even create adaptable areas for older relatives. It's a puzzle, and the pieces need to fit just right. Your real estate agent has the expertise and local knowledge to help you find that home where everyone can be comfortable without breaking the bank. As MoneyGeek.com puts it:

"Having a good multigenerational property can improve the prospects of success when living with loved ones. A multigenerational home should fit the specific needs of most family members regardless of age or health. Speaking to a real-estate agent can help you gain clarity and locate a fit."

Bottom Line

Buying a multi-generational home can be a smart way to tackle some of today’s affordability challenges. When you team up to share expenses, you can make your dream of homeownership more attainable. If this sounds like an option for you and your loved ones, let’s connect to help you find a home that’s the perfect fit.

Planning to Retire? Your Equity Can Help You Make a Move

Reaching retirement is a significant milestone in life, bringing with it a lot of change and new opportunities. As the door to this exciting chapter opens, one thing you may be considering is selling your house and finding a home better suited for your evolving needs.

Fortunately, you may be in a better position to make a move than you realize. Here are a few reasons why.

Consider How Long You’ve Been in Your Home

From 1985 to 2009, the average length of time homeowners stayed in their homes was roughly six years. But according to the National Association of Realtors (NAR), that number is higher today. Since 2010, the average home tenure is just over nine years (see graph below):

This means many homeowners have been living in their houses even longer in recent years. When you live in a home for such a significant amount of time, it’s natural for you to experience changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options waiting for you.

Consider the Equity You’ve Gained

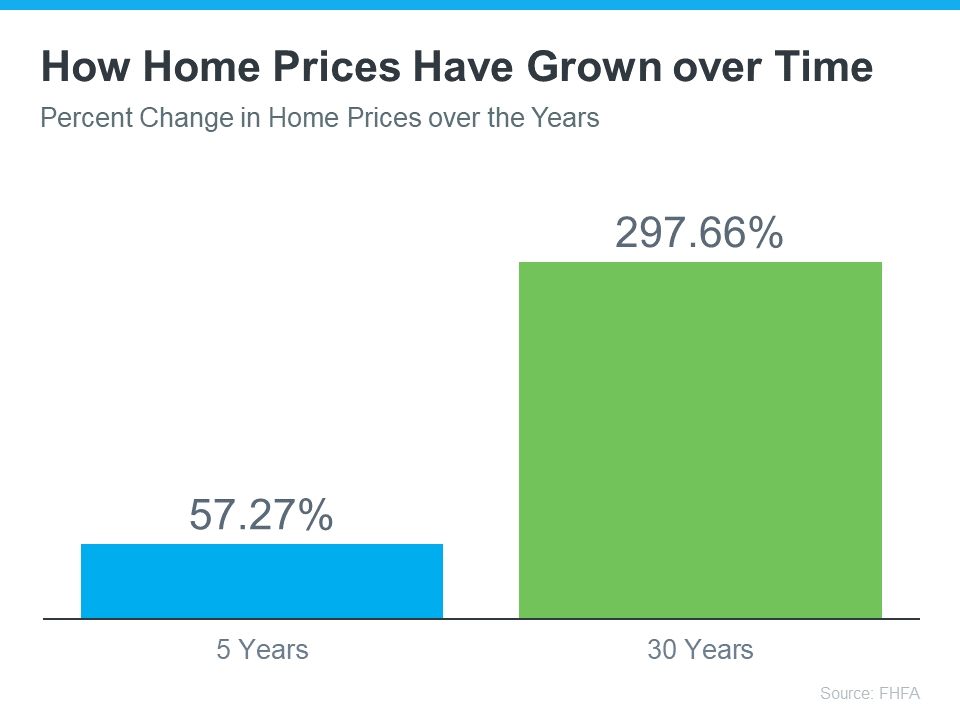

And, if you’ve been in your home for more than a few years, you’ve likely built-up substantial equity that can fuel your next move. That’s because you gain equity as you pay down your loan and as home prices appreciate. And, the longer you’ve been in your home, the more you may have gained. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):

While home prices vary by area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it almost triple in value over that time.

Whether you’re looking to downsize, relocate to a dream destination, or move so you live closer to friends or loved ones, that equity can help. Whatever your home goals are, a trusted real estate agent can work with you to find the best option. They’ll help you sell your current house and guide you as you buy the home that’s right for you and your lifestyle today.

Bottom Line

As you plan for your retirement, let’s connect so we can find out how much equity you’ve built up over the years and plan how you can use it toward the purchase of a home that fits your changing needs.

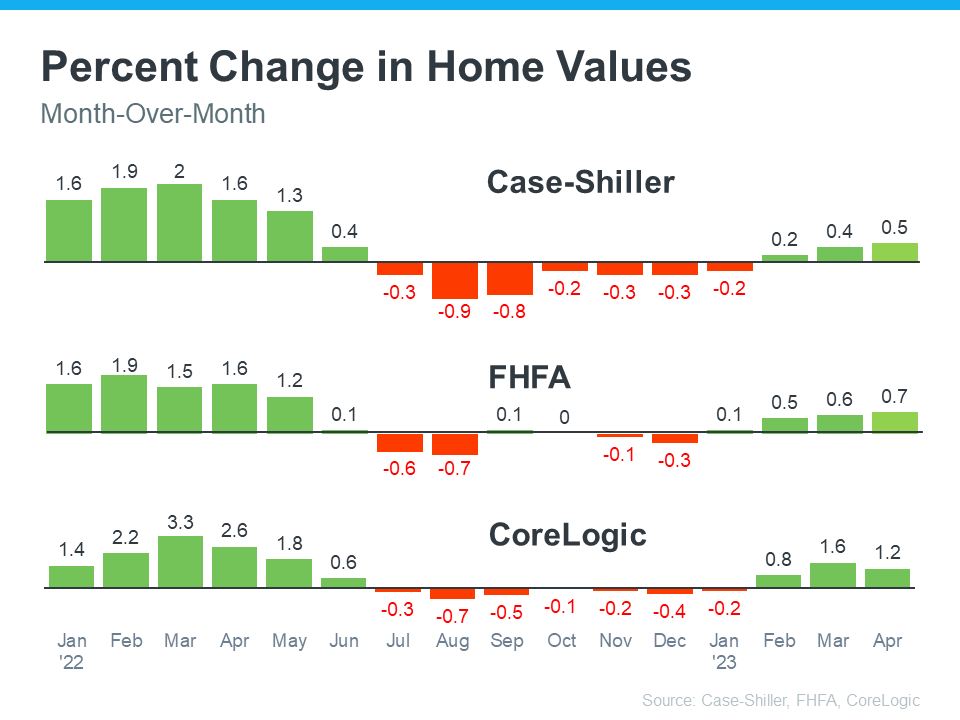

Home Prices Are Rebounding

If you’re following the news today, you may feel a bit unsure about what’s happening with home prices and fear whether or not the worst is yet to come. That’s because today’s headlines are painting an unnecessarily negative picture. If we take a year-over-year view, home prices did drop some, but that’s because we’re comparing to a ‘unicorn’ year when prices peaked well beyond the norm.

To avoid an unfair comparison to that previous peak, we need to look at monthly data. And that tells a very different and much more positive story. While local home price trends still vary by market, here’s what the national data tells us.

The graphs below use recent monthly reports from three sources to show the worst home price declines are already behind us, and prices are appreciating nationally.

Looking at this monthly view, we can see the past year in the housing market can be divided into two parts. In the first half of 2022, home prices were going up, and fast. However, starting in July, prices began to go down (shown in red in the graphs above). By around August or September, the trend started to stabilize. But, looking at the most recent data for early 2023, these graphs also show that prices are going up again.

The fact that all three reports show prices have been going up for three or more straight months is an encouraging sign for the housing market. The month-over-month data indicates a national shift is happening – home prices are rising again.

Craig J. Lazzara, Managing Director at S&P Dow Jones Indices, says this about home price trends:

“If I were trying to make a case that the decline in home prices that began in June 2022 had definitively ended in January 2023, April’s data would bolster my argument.”

Experts believe one of the reasons prices didn’t crash like some expected is because there aren’t enough available homes for the number of people who want to buy them. Even with today’s mortgage rates, there are more people looking to buy than there are homes available for sale.

Mark Fleming, Chief Economist at First American, explains how more demand than supply keeps upward pressure on prices:

“History has shown that higher rates may take the steam out of rising prices, but it doesn’t cause them to collapse entirely. This is especially true in today’s housing market, where the demand for homes continues to outpace supply, keeping the pressure on house prices."

Doug Duncan, Senior VP and Chief Economist at Fannie Mae, states home price growth is exceeding expectations thanks to that high demand:

“. . . housing prices continue to show stronger growth than what was previously expected . . . Housing’s performance is a testimony to the strength of demographic-related demand . . .”

Here’s How This Affects You

Buyers: If you've been holding off on buying because you were worried the value of your home would go down, knowing home prices have bounced back should bring you some relief. It also gives you the opportunity to own something that usually becomes more valuable as time goes on.

Sellers: If you've been waiting to sell your house because you were concerned about how changing home prices would affect its value, it might be a good idea to team up with a real estate agent to list your house. You don't have to wait any longer because the latest data suggests things are turning in your favor.

Bottom Line

If you delayed your moving plans because you were concerned about home prices dropping, the latest data reveals the worst is already over, and prices are appreciating nationally. Let's get in touch so you know what's happening with home prices in our area.

Are Home Prices Going Up or Down? That Depends…

Media coverage about what’s happening with home prices can be confusing. A large part of that is due to the type of data being used and what they’re choosing to draw attention to. For home prices, there are two different methods used to compare home prices over different time periods: year-over-year (Y-O-Y) and month-over-month (M-O-M). Here's an explanation of each.

Year-over-Year (Y-O-Y):

This comparison measures the change in home prices from the same month or quarter in the previous year. For example, if you're comparing Y-O-Y home prices for April 2023, you would compare them to the home prices for April 2022.

Y-O-Y comparisons focus on changes over a one-year period, providing a more comprehensive view of long-term trends. They are usually useful for evaluating annual growth rates and determining if the market is generally appreciating or depreciating.

Month-over-Month (M-O-M):

This comparison measures the change in home prices from one month to the next. For instance, if you're comparing M-O-M home prices for April 2023, you would compare them to the home prices for March 2023.

Meanwhile, M-O-M comparisons analyze changes within a single month, giving a more immediate snapshot of short-term movements and price fluctuations. They are often used to track immediate shifts in demand and supply, seasonal trends, or the impact of specific events on the housing market.

The key difference between Y-O-Y and M-O-M comparisons lies in the time frame being assessed. Both approaches have their own merits and serve different purposes depending on the specific analysis required.

Why Is This Distinction So Important Right Now?

We’re about to enter a few months when home prices could possibly be lower than they were the same month last year. April, May, and June of 2022 were three of the best months for home prices in the history of the American housing market. Those same months this year might not measure up. That means, the Y-O-Y comparison will probably show values are depreciating. The numbers for April seem to suggest that’s what we’ll see in the months ahead (see graph below):

That’ll generate troubling headlines that say home values are falling. That’ll be accurate on a Y-O-Y basis. And, those headlines will lead many consumers to believe that home values are currently cascading downward.

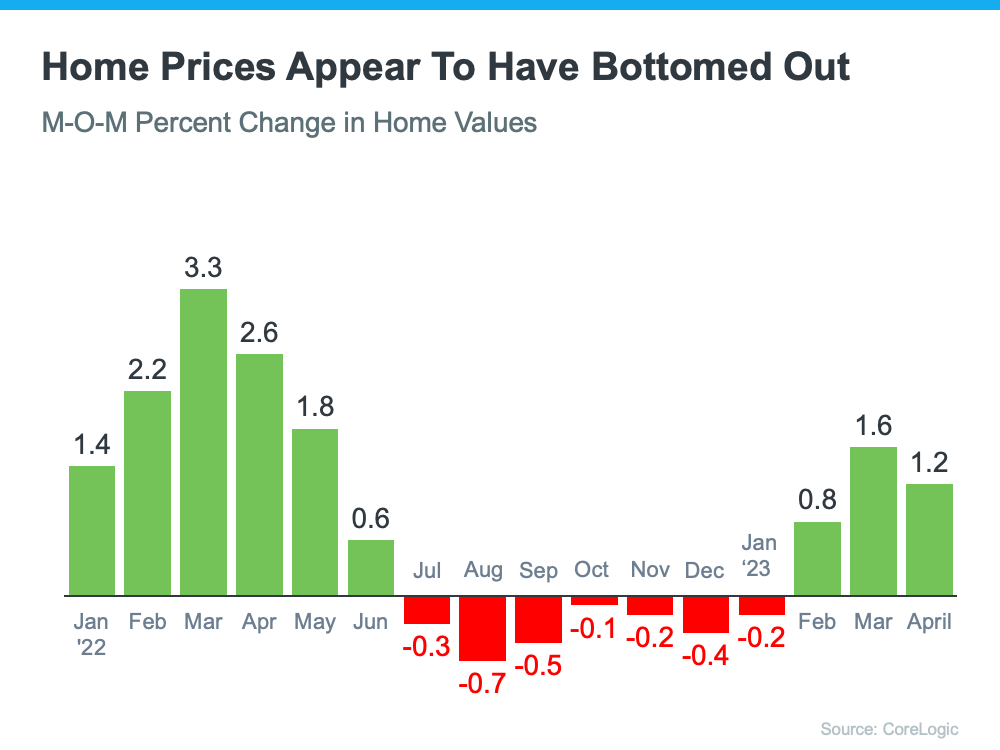

However, on a closer look at M-O-M home prices, we can see prices have actually been appreciating for the last several months. Those M-O-M numbers more accurately reflect what’s truly happening with home values: after several months of depreciation, it appears we’ve hit bottom and are bouncing back.

Here’s an example of M-O-M home price movements for the last 16 months from the CoreLogic Home Price Insights report (see graph below):

Why Does This Matter to You?

So, if you’re hearing negative headlines about home prices, remember they may not be painting the full picture. For the next few months, we’ll be comparing prices to last year’s record peak, and that may make the Y-O-Y comparison feel more negative. But, if we look at the more immediate, M-O-M trends, we can see home prices are actually on the way back up.

There’s an advantage to buying a home now. You’ll buy at a discount from last year’s price and before prices start to pick up even more momentum. It’s called “buying at the bottom,” and that’s a good thing.

Bottom Line

If you have questions about what’s happening with home prices, or if you’re ready to buy before prices climb higher, let’s connect.

Falling out of Love with Your House? It May Be Time To Move.

Owning a home means having a place that’s solely your own and provides the space, features, and location you and your loved ones need. But what happens when your needs change? If this hits home for you, it may be time to make a move.

According to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), the average person has lived in their current house for ten years. If you’ve been in your home for a while, think about how much in your life has changed since you moved in. Even if you thought it would be your forever home when you bought it, it doesn’t have to be. Work with a local real estate agent to explore all your options in today’s market before settling for your current home.

That’s actually what a lot of homeowners are doing right now. A recent survey from Realtor.com finds that, of people who are considering selling in 2023, one in three are thinking about moving because their home no longer meets their needs. And according to the same report from NAR, that’s consistent with this year’s top reasons for selling, which include:

Want to move closer to friends or family

Moving due to retirement

Home is too small or too large

Change in family situation

Job relocation

If things in your life have changed, it may be time to make a move. And there’s good news: it’s still a great time to sell. Here’s why.

We’re in a strong sellers’ market. That means homes listed at market value and in good condition are getting attention from buyers and selling quickly. Lean on your expert real estate advisor for the best advice on getting your house ready to sell.

Your equity can power your next move. There’s a good chance you have a significant amount of equity right now thanks to record levels of price appreciation in recent years. When you sell, you can use that equity to help afford your next home. In fact, NAR’s report from above shows 38% of recent buyers used the money from the sale of their previous home to cover the down payment on their next one. Work with a local real estate agent to learn how much equity you have and what you can do with it in today’s housing market.

Bottom Line

If your home no longer meets your needs, consider selling it so you can find your dream home. Let’s connect so you can learn about your options.

Get Ready: The Best Time To List Your House Is Almost Here

If you’re thinking about selling this spring, it’s time to get moving – the best week to list your house is fast approaching.

Experts at realtor.com looked at seasonal trends from recent years (excluding 2020 as an uncharacteristic year due to the onset of the pandemic) and determined the ideal week to list a house this year:

“Home sellers on the fence waiting for that perfect moment to sell should start preparations, because the best time to list a home in 2023 is approaching quickly. The week of April 16-22 is expected to have the ideal balance of housing market conditions that favor home sellers, more so than any other week in the year.”

If you’ve been waiting for the best time to sell, this is your chance. But remember, before you put your house on the market, you’ve got to get it ready. And if you haven’t started that process yet, you’ll need to move quickly. Here’s what you should keep in mind.

Work with an Agent To Determine Which Updates To Make

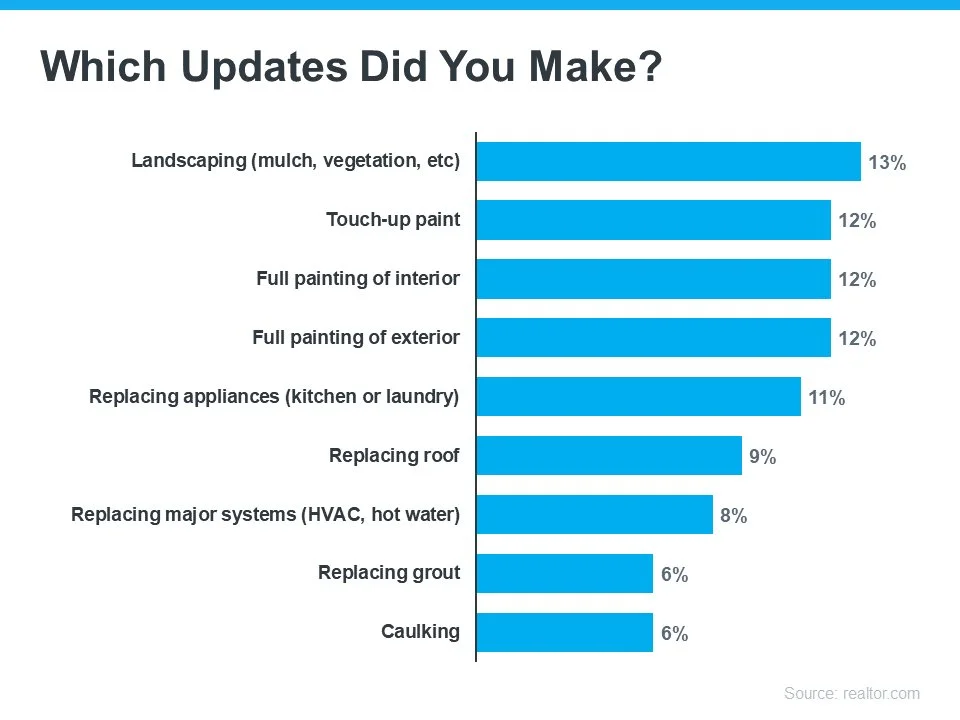

Start by prioritizing which updates you’ll make. In February, realtor.com asked more than 1,200 recent or potential home sellers what updates they ended up making to their house before listing it (see graph below):

As you can see, the most common answers included landscaping and painting. Work with a trusted real estate agent to determine what projects make the most sense for your goals and local market.

If Possible, Plan To Have Your House Staged

Once you’ve made any necessary repairs and updates to your house, consider having it staged. According to the National Association of Realtors (NAR), 82% of buyers’ agents said staging a home made it easier for a buyer to visualize the property as a future home. Additionally, almost half of buyers’ agents said home staging had an effect on most buyers’ view of the home in general. Homes that are staged typically sell faster and for a higher price because they help potential buyers more easily picture their new life in the house.

Bottom Line

Are you ready to sell this spring? Let’s connect to plan your next steps. You can start by making a checklist of what you think your house needs to get ready. Then, we can work together to prioritize your list and move forward together.

Think Twice Before Waiting for 3% Mortgage Rates

Last year, the Federal Reserve took action to try to bring down inflation. In response to those efforts, mortgage rates jumped up rapidly from the record lows we saw in 2021, peaking at just over 7% last October. Hopeful buyers experienced a hit to their purchasing power as a result, and some decided to press pause on their plans.

Today, the rate of inflation is starting to drop. And as a result, mortgage rates have dipped below last year’s peak. Sam Khater, Chief Economist at Freddie Mac, shares:

“While mortgage market activity has significantly shrunk over the last year, inflationary pressures are easing and should lead to lower mortgage rates in 2023.”

That’s potentially great news if you’re a buyer aiming to jump back into the housing market. Any drop in mortgage rates helps boost your purchasing power by bringing down your expected monthly mortgage payment. This means the lower mortgage rates experts forecast this year could be just what you need to reignite your homebuying goals.

While this opens up a window of opportunity for you, remember: you shouldn’t expect rates to drop back down to record lows like we saw in 2021. Experts agree that’s not the range buyers should bank on. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“I think we could be surprised at how much mortgage rates pull back this year. But we’re not going back to 3 percent anytime soon, because inflation is not going back to 2 percent anytime soon.”

It’s important to have a realistic vision for what you can expect this year, and that’s where the advice of expert real estate advisors is critical. You may be surprised by the impact even a mild drop in mortgage rates has on your budget. If you’re ready to buy a home now, today’s market presents the opportunity to get a more affordable mortgage rate, find your dream home, and face less competition from other buyers.

Bottom Line

The recent pullback in mortgage rates is great news – but if you’re ready to buy now, holding out for 3% is a mistake. Work with a local lender to learn how today’s rates impact your goals, and let’s connect to explore your options in our area.

What Are Your Goals in the Housing Market This Year?

If buying or selling a home is part of your dreams for 2023, it’s essential for you to understand today’s housing market, define your goals, and work with industry experts to bring your homeownership vision for the new year into focus.

In the last year, high inflation had a big impact on the economy, the housing market, and likely on your wallet too. That’s why it’s critical to have a clear understanding of not just the market today, but also what you want out of it when you buy or sell a home. Danielle Hale, Chief Economist at realtor.com, explains:

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, so that you can stay in your home long enough that buying is a sound financial decision.”

Here are a few questions you can start thinking through as you fine tune your goals for 2023.

1. What’s Motivating You?

You’re dreaming about making a move for a reason – what is it? No matter what’s happening in the market, there are still many compelling reasons to buy a home today. Your needs may have changed in a way your current house can’t address, or you could be ready to step into homeownership for the first time and have a space that’s truly your own. Use what’s motivating you as a guidepost in partnership with an expert advisor to help make sure your move will give you a lasting sense of accomplishment.

2. What Does Your Next Home Look Like?

You know you want to move, but how would you describe your dream home? The available supply of homes for sale has grown, and that could mean more options to choose from when you buy. Just be sure to keep your budget in mind and work with a trusted real estate professional to balance your wants and needs. The better you understand what’s essential and where you can be flexible, the easier it can be to find the home that’s right for you.

3. How Ready Are You To Buy?

Getting clear on your budget and savings is essential before you get too far into the process. Working with a local agent and a lender early is the best way to make sure you’re in a good position to buy. This could include planning how much to save for a down payment, getting pre-approved for a home loan, and assessing your current home equity if your move involves selling your existing house.

A Professional Will Guide You Through Every Step of the Process

Buying or selling a home is a big process that takes expertise to navigate. If that feels a bit overwhelming, you aren’t alone. According to a recent Harris Poll survey, one in five respondents see a lack of information or knowledge about the homebuying process as a barrier from owning a home. Don’t let uncertainty hold you back from your goals this year. A trusted expert can bridge that gap and give you the best advice and information about today’s market.

Bottom Line

Let’s connect to plan how your dreams for 2023 can become a reality.

3 Ways You Can Use Your Home Equity

If you’re a homeowner, odds are your equity has grown significantly over the last few years as home prices skyrocketed and you made your monthly mortgage payments. Home equity builds over time and can help you achieve certain goals. According to the latest Equity Insights Report from CoreLogic, the average borrower with a home loan has almost $300,000 in equity right now.

As you weigh your options, especially in the face of inflation and talk of a recession, it’s important to understand your assets and how you can leverage them. A real estate professional is the best resource to help you understand how much home equity you have and advise you on some of the ways you can use it. Here are a few examples.

1. Buy a Home That Fits Your Needs

If you no longer have the space you need, it might be time to move into a larger home. Or it’s possible you have too much space and need something smaller. No matter the situation, consider using your equity to power a move into a home that fits your changing lifestyle.

If you want to upgrade your house, you can put your equity toward a down payment on the home of your dreams. And if you’re planning to downsize, you may be surprised that your equity may cover some, if not all, of the cost of your next home. A real estate advisor can help you figure out how much equity you have and how you can use it toward the purchase of your next home.

2. Reinvest in Your Current House

According to a recent survey from Point, 39% of homeowners would invest in home improvement projects if they chose to access their equity. This is a great option if you want to change some things about your living space but you aren’t ready to make a move just yet.

Home improvement projects allow you to customize your home to suit your needs and sense of style. Just remember to think ahead with any updates you make, as some renovations add more value to your home and are more likely to appeal to future buyers than others. For example, a report from the National Association of Realtors (NAR) shows refinishing or replacing wood flooring has a high cost recovery. Lean on a local professional for the best advice on which projects to invest in to get the greatest return on your investment when you sell.

3. Pursue Your Personal Goals

In addition to making a move or updating your house, home equity can also help you achieve the life goals you’ve dreamed of. That could mean investing in a new business venture, retiring or downsizing, or funding an education. While you shouldn’t use your equity for unnecessary spending, leveraging it to start a business or putting it toward education costs can help you achieve other lifelong goals.

Bottom Line

Your equity can be a game changer. If you’re unsure how much equity you have in your home, let’s connect so you can start planning your next move.

What’s Ahead for Home Prices?

As the housing market cools in response to the dramatic rise in mortgage rates, home price appreciation is cooling as well. And if you’re following along with headlines in the media, you’re probably seeing a wide range of opinions calling for everything from falling home prices to ongoing appreciation. But what’s true? What’s most likely to happen moving forward?

While opinions differ, the most likely outcome is we’ll fall somewhere in the middle of slight appreciation and slight depreciation. Here’s a look at the latest expert projections so you have the best information possible today.

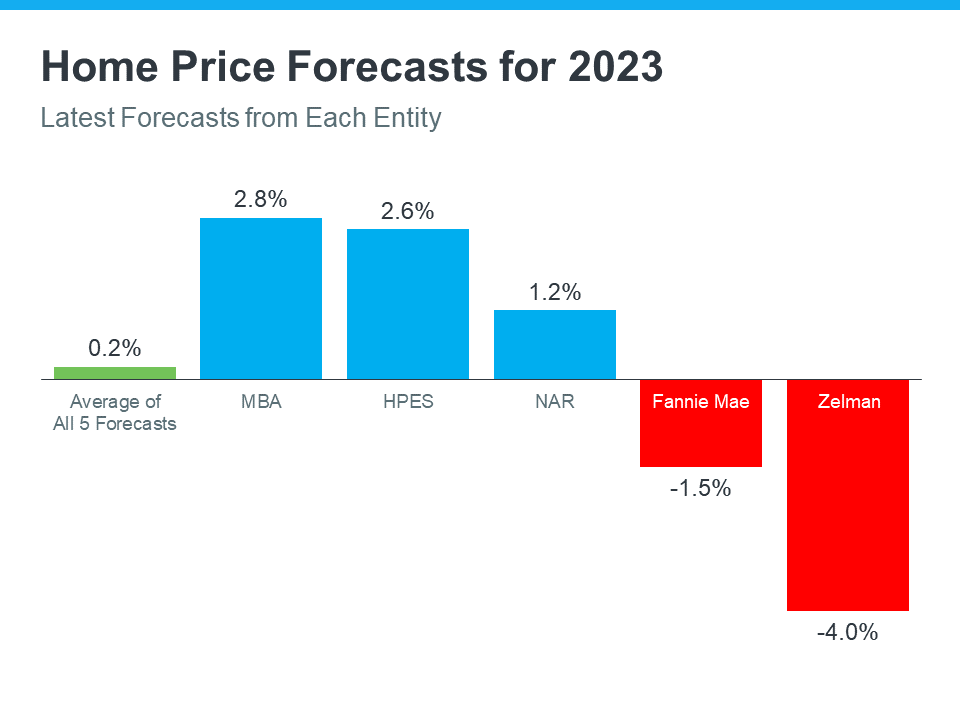

What the Experts Are Saying About Home Prices Next Year

The graph below shows the most up-to-date forecasts from five experts in the housing industry. These are the experts that have most recently updated their projections based on current market trends:

As the graph shows, the three blue bars represent experts calling for ongoing home price appreciation, just at a more moderate rate than recent years. The red bars on the graph are experts calling for home price depreciation.

While there isn’t a clear consensus, if you take the average (shown in green) of all five of these forecasts, the most likely outcome is, nationally, home price appreciation will be fairly flat next year.

What Does This Mean?

Basically, experts are divided on what’s ahead for 2023. Home prices will likely depreciate slightly in some markets and will continue to gain ground in others. It all depends on the conditions in your local market, like how overheated that market was in recent years, current inventory levels, buyer demand, and more.

The good news is home prices are expected to return to more normal levels of appreciation rather quickly. The latest forecast from Wells Fargo shows that, while they feel prices will fall in 2023, they think prices will recover and net positive in 2024. That forecast calls for 3.1% appreciation in 2024, which is a number much more in line with the long-term average of 4% annual appreciation.

And the Home Price Expectation Survey (HPES) from Pulsenomics, a poll of over one hundred industry experts, also calls for ongoing appreciation of roughly 2.6 to 4% from 2024-2026. This goes to show, even if prices decline slightly next year, it’s not expected to be a lasting trend.

As Jason Lewris, Co-Founder and Chief Data Officer for Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

Don’t let fear or uncertainty change your plans. If you’re unsure about where prices are headed or how to make sense of what’s going on in today’s housing market, reach out to a local real estate professional for the guidance you need each step of the way.

Bottom Line

The housing market is shifting, and it’s a confusing place right now. Let’s connect so you have a trusted real estate professional to help you make confident and informed decisions about what’s happening in our market.

The Cost of Waiting for Mortgage Rates To Go Down

Mortgage rates have increased significantly in recent weeks. And that may mean you have questions about what this means for you if you’re planning to buy a home. Here’s some information that can help you make an informed decision when you set your homebuying plans.

The Impact of Rising Mortgage Rates

As mortgage rates rise, they impact your purchasing power by raising the cost of buying a home and limiting how much you can comfortably afford. Here’s how it works.

Let’s assume you want to buy a $400,000 home (the median-priced home according to the National Association of Realtors is $389,500). If you’re trying to shop at that price point and keep your monthly payment about $2,500-2,600 or below, here’s how your purchasing power can change as mortgage rates climb (see chart below). The red shows payments above that threshold and the green indicates a payment within your target range.

As the chart shows, as rates go up, the amount you can afford to borrow decreases and that may mean you have to look at homes at a different price point. That’s why it’s important to work with a real estate advisor to understand how mortgage rates impact your monthly mortgage payment at various home loan amounts.

Are Mortgage Rates Going To Go Down?

The rise in mortgage rates and the resulting decrease in purchasing power may leave you wondering if you should wait for rates to go down before making your purchase. Realtor.com says this about where rates could go from here:

“Many homebuyers likely winced . . . upon hearing that the Federal Reserve yet again boosted its short-term interest rates by three-quarters of a percentage point—a move that’s pushing mortgage rates through the roof. And the already high rates are just going to get higher.”

So, if you’re waiting for mortgage rates to drop, you may be waiting for a while as the Federal Reserve works to get inflation under control.

And if you’re considering renting as your alternative while you wait it out, remember that’s going to get more expensive with time too. As Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says:

“There is no doubt that these higher rates hurt housing affordability. Nevertheless, apart from borrowing costs, rents additionally rose at their highest pace in nearly four decades.”

Basically, it is true that it costs more to buy a home today than it did last year, but the same is true for renting. This means, either way, you’re going to be paying more. The difference is, with homeownership, you’re also gaining equity over time which will help grow your net worth. The question now becomes: what makes more sense for you?

Bottom Line

Each person’s situation is unique. To make the best decision for you, let’s connect to explore your options.

Buyers: You May Face Less Competition as Bidding Wars Ease

One of the top stories in recent real estate headlines was the intensity and frequency of bidding wars. With so many buyers looking to purchase a home and so few of them available for sale, fiercely competitive bidding wars became the norm during the pandemic – and it drove home prices up. If you tried to buy a house over the past two years, you probably experienced this firsthand and may have been outbid on several homes along the way.

But here’s the news you’ve been waiting for: data shows clear signs bidding wars are easing this year.

According to the National Association of Realtors (NAR), the average number of offers on recently sold homes has declined considerably over the past few months (see graph below):

The graph shows homes were seeing a high of around five offers earlier this year. But the latest data shows that average was down to just shy of three offers per recently sold home. This shift is happening largely because rising mortgage rates moderated buyer demand and slowed home sales, resulting in a growing supply of homes on the market. Essentially, more choices for buyers.

What This Means for You

If you put your home search on pause because you were outbid last year or because you didn’t want to deal with the peak intensity of bidding wars, you can breathe a welcome sigh of relief. While it’s still a sellers’ market, an uptick in inventory gives you a window of opportunity to jump back in. You may still be competing with some buyers, but it likely won’t be anything like it was just a few short months ago.

Bottom Line

If you put your plans on pause because of intense bidding wars in recent years, it may be time to kick off your home search. Today, bidding wars are easing and that may mean less competition for you as a buyer. If you’re serious about buying a home or making a move, let’s connect to get started today.

What’s Causing Ongoing Home Price Appreciation?

If you’re thinking about making a move, you probably want to know what’s going to happen to home prices for the rest of the year. While experts say price growth will moderate due to the shifting market, ongoing appreciation is expected. That means home prices won’t fall. Here’s a look at two key reasons experts forecast continued price growth: supply and demand.

While Growing, Housing Supply Is Still Low

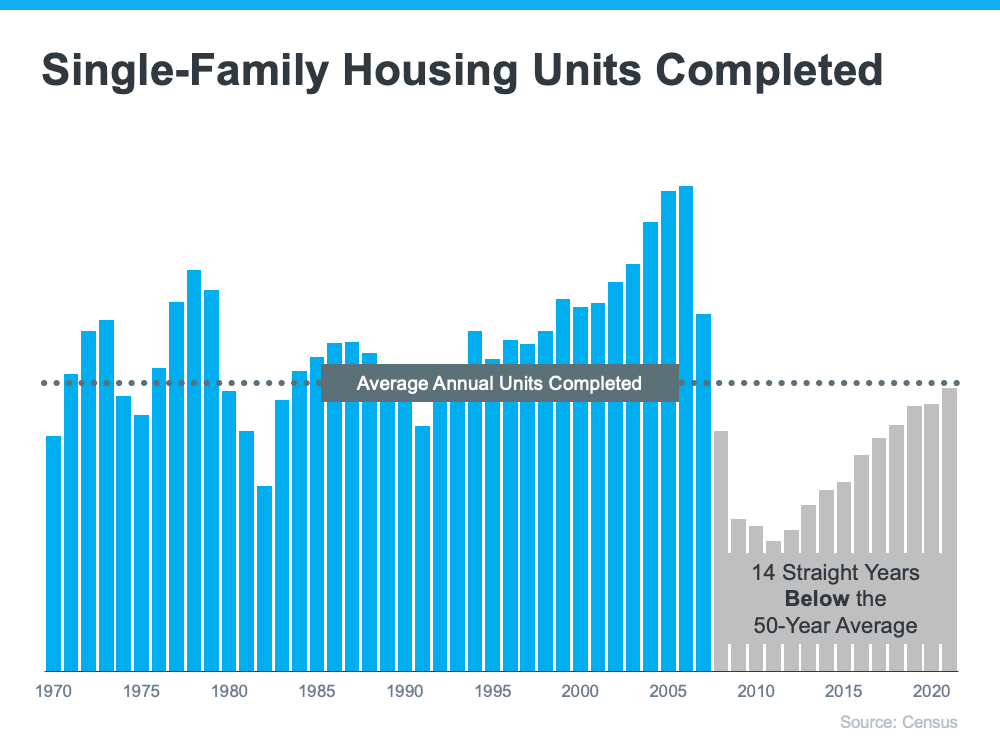

Even though inventory is increasing this year as the market moderates, supply is still low. The graph below helps tell the story of why there still aren’t enough homes on the market today. It uses data from the Census to show the number of single-family homes that were built in this country going all the way back to the 1970s.

The blue bars represent the years leading up to the housing crisis in 2008. As the graph shows, right before the crash, homebuilding increased significantly. That’s because buyer demand was so high due to loose lending standards that enabled more people to qualify for a home loan.

The resulting oversupply of homes for sale led to prices dropping during the crash and some builders leaving the industry or closing their businesses – and that led to a long period of underbuilding of new homes. And even as more new homes are constructed this year and in the years ahead, this isn’t something that can be resolved overnight. It’ll take time to build enough homes to meet the deficit of underbuilding that took place over the past 14 years.

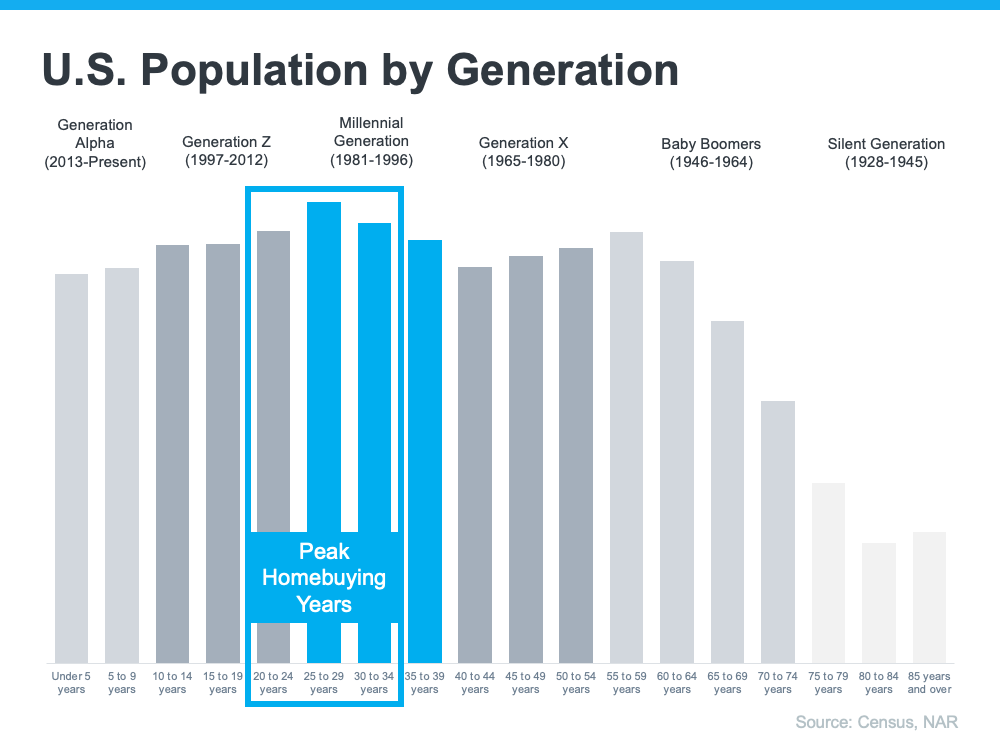

Millennials Will Create Sustained Buyer Demand Moving Forward

The frenzy the market saw during the pandemic is because there was more demand than homes for sale. That drove home prices up as buyers competed with one another for available homes. And while buyer demand has moderated today in response to higher mortgage rates, data tells us demand will continue to be driven by the large generation of millennials aging into their peak homebuying years (see graph below):

Odeta Kushi, Deputy Chief Economist at First American, explains:

“. . . millennials continue to transition to their prime home-buying age and will remain the driving force in potential homeownership demand in the years ahead.”

That combination of millennial demand and low housing supply continues to put upward pressure on home prices. As Bankrate says:

“After all, supplies of homes for sale remain near record lows. And while a jump in mortgage rates has dampened demand somewhat, demand still outpaces supply, thanks to a combination of little new construction and strong household formation by large numbers of millennials.”

What This Means for Home Prices

If you’re worried home values will fall, rest assured that experts forecast ongoing home price appreciation thanks to the lingering imbalance of supply and demand. That means home prices won’t decline.

Bottom Line

Based on today’s factors driving supply and demand, experts project home price appreciation will continue. It’ll just happen at a more moderate pace as the housing market continues its shift back toward pre-pandemic levels.

Homeownership Is a Great Hedge Against the Impact of Rising Inflation

If you’re following along with the news today, you’ve heard about rising inflation. Today, inflation is at a 40-year high. According to the National Association of Home Builders (NAHB):

“Consumer prices accelerated again in May as shelter, energy and food prices continued to surge at the fastest pace in decades. This marked the third straight month for inflation above an 8% rate and was the largest year-over-year gain since December 1981.”

With inflation rising, you’re likely feeling it impact your day-to-day life as prices go up for gas, groceries, and more. These climbing consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Helps You Stabilize One of Your Biggest Monthly Expenses

Investopedia explains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. When you have a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same. That’s certainly not the case if you’re renting.”

So even if other prices increase, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

Investing in an Asset That Historically Outperforms Inflation

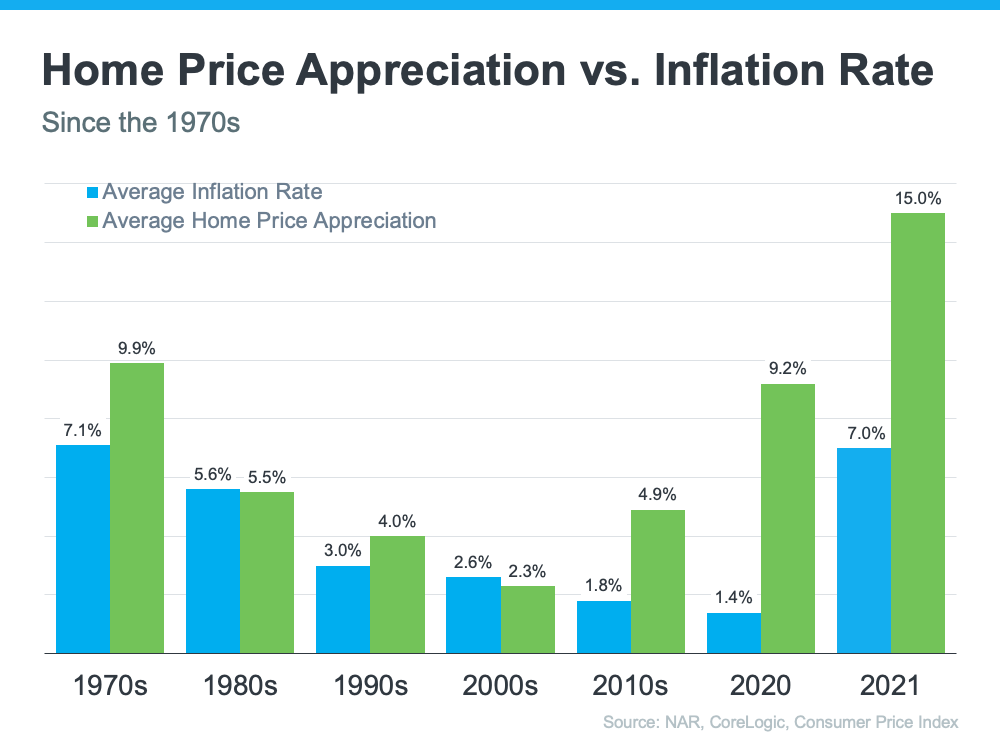

While it’s true rising home prices and higher mortgage rates mean that buying a house today costs more than it did even a few months ago, you still have an opportunity to set yourself up for a long-term win. That’s because, in inflationary times, you want to be invested in an asset that outperforms inflation and typically holds or grows in value.

The graph below shows how the average home price appreciation outperformed the average inflation rate in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts forecast home prices will only go up from here thanks to the ongoing imbalance of supply and demand. Once you buy a house, any home price appreciation that does occur will grow your equity and your net worth. And since homes are typically assets that grow in value, you have peace of mind that history shows your investment is a strong one.

That means, if you’re ready and able, it makes sense to buy today before prices rise further.

Bottom Line

If you’ve been thinking about buying a home this year, it makes sense to act soon, even with inflation rising. That way you can stabilize your monthly housing cost and invest in an asset that historically outperforms inflation. If you’re ready to get started, let’s connect so you have expert advice on your specific situation when you’re ready to buy a home.

Why Summer Is a Great Time To Buy a Vacation Home

You may be someone who looks forward to summer each year because it gives you an opportunity to rest, unwind, and enjoy more quality time with your loved ones. Now that summer is just around the corner, it’s worthwhile to start thinking about your plans and where you want to spend your vacations this year. Here are a few reasons a vacation home could be right for you.

Why You May Want To Consider a Vacation Home Today

Over the past two years, a lot has changed. You may be one of many people who now work from home and have added flexibility in where you live. You may also be someone who delayed trips for personal or health reasons. If either is true for you, there could be a unique opportunity to use the flexibility that comes with remote work or the money saved while not traveling to invest in your future by buying a vacation home.

Bankrate explains why a second home, or a vacation home, may be something worth considering:

“For those who are able, buying a second home is suddenly more appealing, as remote working became the norm for many professionals during the pandemic. Why not work from the place where you like to vacation — the place where you want to live?

If you don’t work remotely, a vacation home could still be at the top of your wish list if you have a favorite getaway spot that you visit often. It beats staying in a tiny hotel room or worrying about rental rates each time you want to take a trip.”

How a Professional Can Help You Find the Right One

So, if you’re looking for an oasis, you may be able to make it a second home rather than just the destination for a trip. If you could see yourself soaking up the sun in a vacation home, you may want to start your search. Summer is a popular time to buy vacation homes. By beginning the process now, you could get ahead of the competition.

The first step is working with a local real estate advisor who can help you find a home in your desired location. A professional has the knowledge and resources to help you understand the market, what homes are available and at what price points, and more. They can also walk you through all the perks of owning a second home and how it can benefit you.

A recent article from the National Association of Realtors (NAR), mentions some of the top reasons buyers today are looking into purchasing a second, or a vacation, home:

“According to Google’s data, the top reasons that homeowners cited for purchasing a second home were to diversify their investments, earn money renting, and use as a vacation home.”

If any of the reasons covered here resonate with you, connect with a real estate professional to learn more. They can give you expert advice based on what you need, your goals, and what you’re hoping to get out of your second home.

Bottom Line

Owning a vacation home is an investment in your future and your lifestyle. If this is one of your goals this year, you still have time to buy and enjoy spending the summer in your vacation home. When you’re ready to get started, let’s connect.

Today’s Home Price Appreciation Is Great News for Existing Homeowners

If you’re planning to sell your home this season, rising prices are great news for you. But it’s important to understand why prices are rising to begin with. One major factor is supply and demand.

In any industry, when there are more buyers for an item than there are of that item available, prices naturally rise. In those situations, buyers are willing to pay more to get the product or service they’re looking for when options are scarce. And that’s exactly what’s happening in the current real estate market.

Selma Hepp, Executive, Research & Insights and Deputy Chief Economist at CoreLogic, puts it like this:

“With so few homes, buyers are once again left with fierce competition that’s driving the share of homes that sold over the listing price up to 66% . . . With the continued imbalance between supply and demand, home prices are likely to have another year of strong gains and are expected to average about 10% growth for the year.”

Because it will take some time for housing supply to increase, experts believe prices will continue rising. The latest Home Price Expectations Survey forecasts what will happen with home prices over the next 5 years. As the graph below shows, while the rate of appreciation will moderate over the next few years, prices will continue rising through 2026:

What This Means When You Sell Your House

If you’re a homeowner, the projection for continued price appreciation this year opens up an opportunity to move. That’s because it may give your equity a major boost. Equity is the difference between what you owe on your house and its market value. The amount of equity you have increases as you make your monthly payments and as rising home prices drive up the market value for your home.

Growing equity is a powerful tool for homeowners. When you sell your house, the equity you’ve built comes back to you in the sale. That money could be enough to cover some (if not all) of your down payment on your next home.

Of course, if you want to know how much equity you have in your current house, it’s crucial to work with a real estate professional. They follow current market trends and can help you understand your home’s value when you’re ready to sell.

What This Means for Your Next Purchase

But today’s rising home values aren’t just good news if you’re ready to sell. Because price appreciation is forecast to continue in the years ahead, you can rest assured your next home will be an investment that should grow in value with time. That’s one of several reasons why real estate has been rated the best investment in a recent Gallup poll.

Bottom Line

If you’re weighing whether or not you should sell your house this season, know rising home values may be opening up an opportunity to use equity to fuel your move. Let’s connect so you can find out how much your home is worth and to learn more about all the benefits you have in today’s market.

What You Can Expect from the Spring Housing Market

As the spring housing market kicks off, you likely want to know what you can expect this season when it comes to buying or selling a house. While there are multiple factors causing some uncertainty, including the conflict overseas, rising inflation, and the first rate increase from the Federal Reserve in over three years — the housing market seems to be relatively immune.

Here’s a look at what experts say you can expect this spring.

1. Mortgage Rates Will Climb

Freddie Mac reports the 30-year fixed mortgage rate has increased by more than a full point in the past six months. And despite some mild fluctuation in recent weeks, experts believe rates will continue to edge up over the next 90 days. As Freddie Mac says:

“The Federal Reserve raising short-term rates and signaling further increases means mortgage rates should continue to rise over the course of the year.”

If you’re a first-time buyer or a seller thinking of moving to a home that better fits your needs, realize that waiting will likely mean you’ll pay a higher mortgage rate on your purchase. And that higher rate drives up your monthly payment and can really add up over the life of your loan.

2. Housing Inventory Will Increase

There may be some relief coming for buyers searching for a home to purchase. Realtor.com recently reported that the number of newly listed homes has grown for each of the last two months. Also, the National Association of Realtors (NAR) just announced the months’ supply of inventory increased for the first time in eight months. The inventory of existing homes usually grows every spring, and it seems, based on recent activity, the next 90 days could bring more listings to the market.

If you’re a buyer who has been frustrated with the limited supply of homes available for sale, it looks like you could find some relief this spring. However, be prepared to act quickly if you find the right home.

If you’re a seller, listing now instead of waiting for this additional competition to hit the market makes sense. Your leverage in any negotiation during the sale will be impacted as additional homes come to market.

3. Home Prices Will Rise

Prices are always determined by supply and demand. Though the number of homes entering the market is increasing, buyer demand remains very strong. As realtor.com explains in their most recent Housing Report:

“During the final two weeks of the month, more new sellers entered the market than during the same time last year. . . . However, with 5.8 million new homes missing from the market and millions of millennials at first-time buying ages, housing supply faces a long road to catching up with demand.”

What does that mean for you? With the demand for housing still outpacing supply, home prices will continue to appreciate. Many experts believe the level of appreciation will decelerate from the high double-digit levels we’ve seen over the last two years. That means prices will continue to climb, just at a more moderate pace. Most experts are predicting home prices will not depreciate.

Won’t Increasing Mortgage Rates Cause Home Prices To Fall?

While some people may believe a 1% increase in mortgage rates will impact demand so dramatically that home prices will have to fall, experts say otherwise. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, says:

“What I will caution against is making the inference that interest rates have a direct impact on house prices. That is not true.”

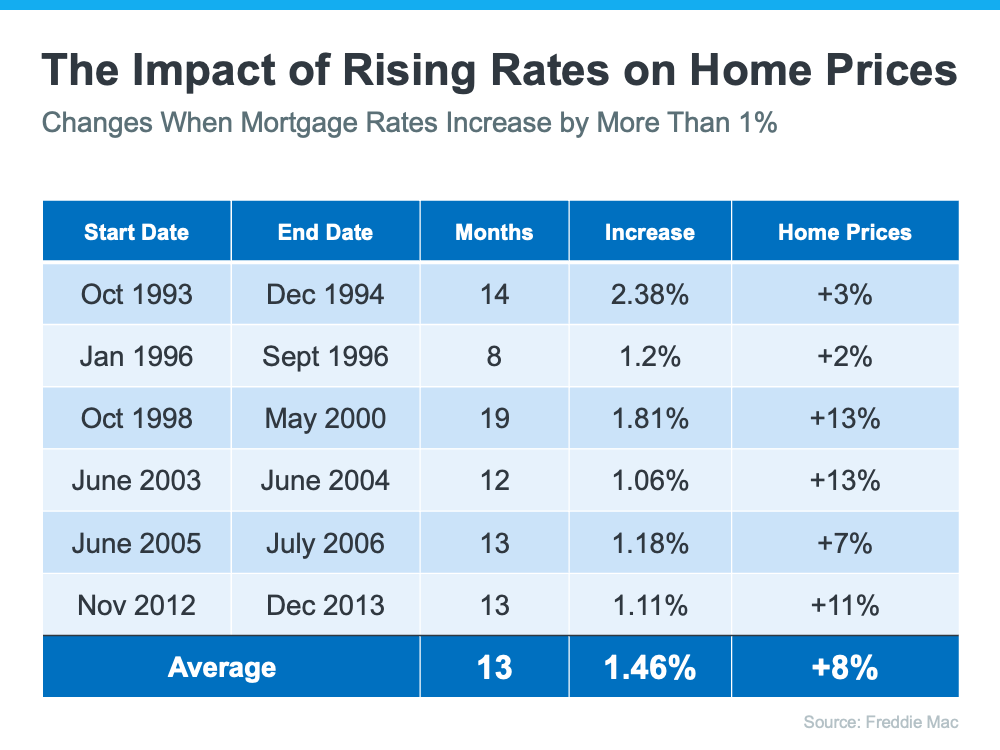

Freddie Mac studied the impact that mortgage rates increasing by at least 1% has had on home prices in the past. Here are the results of that study:

As the chart shows, mortgage rates jumped by at least 1% six times in the last thirty years. In each case, home values increased.

So again, if you’re a first-time buyer or a repeat buyer, waiting to buy likely means you’ll pay more for a home later in the year (as compared to its current value).

Bottom Line

There are three things that seem certain going into the spring housing market:

Mortgage rates will continue to rise

The selection of homes available for sale will modestly improve

Home prices will continue to appreciate, just at a slightly slower pace

If you’re thinking of buying, act now before mortgage rates and home prices increase further. If you’re thinking of selling, your best bet may be to sell soon so you can beat the increase in competition that’s about to come to market.

How To Navigate a Market Where Multiple Offers Is the New Normal

If you’re thinking of buying a home today, you already know that the number of homes available for sale is low. But what does that really mean for you? As a buyer, low housing supply coupled with high buyer demand means you should be prepared to navigate a highly competitive market where homes sell fast and get multiple offers. Realtor.com has this to say:

“Homes also flew off the market at record pace as buyers put offers in the moment properties came up for sale….”

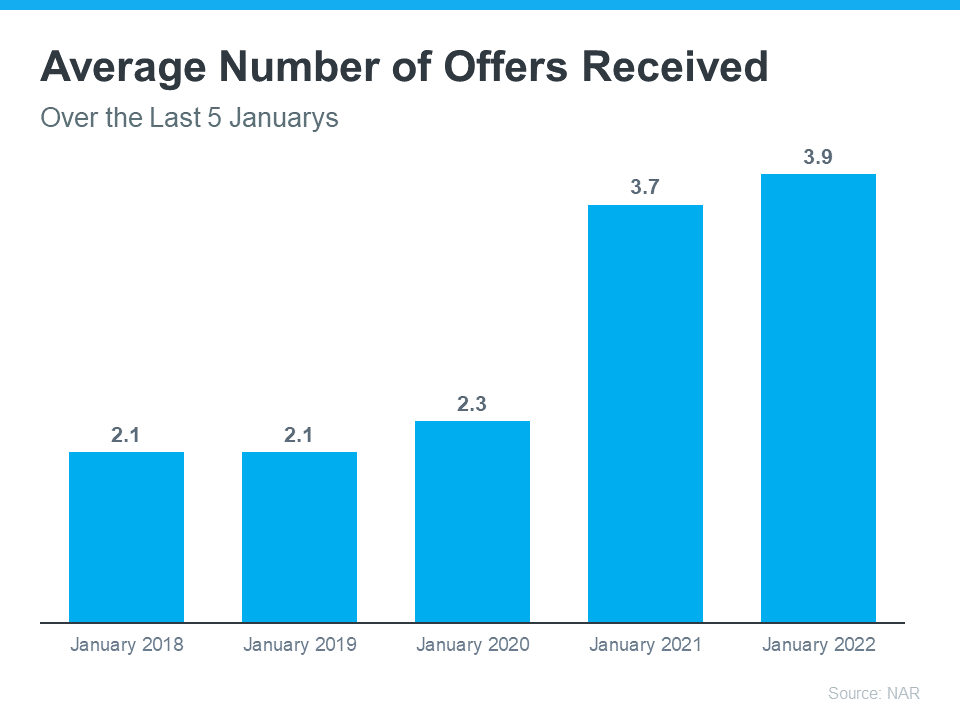

In a bidding war situation like this, doing everything you can to get ahead of the competition is a wise move. That’s because when you find a house and submit an offer, it’ll likely be up against strong offers from other buyers. According to the latest Realtors Confidence Index from the National Association of Realtors (NAR), homes today are receiving an average of 3.9 offers. That’s the most offers we’ve seen in January for the last 5 years (see graph below):

To help you navigate bidding wars with multiple offers, an expert real estate advisor is key. They know what’s worked for other buyers, what sellers are looking for, and how to help you prepare when it comes time to make an offer. Here are three tips to keep in mind that will help you make the best offer possible.

1. Know Your Numbers

Knowing your budget and what you can afford is critical to your success as a homebuyer. The best way to understand your numbers is to work with a lender so you can get pre-approved for a loan. Pre-approval shows sellers you’re serious, which can give you a competitive edge. You should also know making an offer at the home’s asking price may not be enough. Homes today often sell for more than their listing price. An agent can help you understand the market value of the home and what other homes are selling for in your area.

2. Be Ready To Move Fast

Speed and the pace of sales are contributing factors to today’s competitive housing market. When homes are selling fast, it’s important to stay on top of the market and be ready to move quickly. Your agent will help you stay up to date on the latest listings and help you put together your best offer as soon as you find the home you want to buy.

3. Make a Strong but Fair Offer

When you’re up against other offers, putting your best offer forward from the start is key. Lean on your agent to write a strong offer and use their expertise on which levers you can pull to make your offer as enticing as possible. One option is to wave some of your contract contingencies (conditions you set that the seller must meet for the purchase to be finalized). Just remember there are certain contingencies you don’t want to give up, like the home inspection.

Bottom Line

No matter what, your agent is your best resource for making an offer that stands out in a competitive market. Let’s connect to talk through what you can expect as a buyer and how to kick off a successful home search.

Why Right Now Is a Once-in-a-Lifetime Opportunity for Sellers

If you’re thinking about selling your house in 2022, you truly have a once-in-a-lifetime opportunity at your fingertips. When selling anything, you always hope for strong demand for the item coupled with a limited supply. That maximizes your leverage when you’re negotiating the sale. Home sellers are in that exact situation right now. Here’s why.

Demand Is Very Strong

According to the latest Existing Home Sales Report from the National Association of Realtors (NAR), 6.18 million homes were sold in 2021. This was the largest number of home sales in 15 years. Lawrence Yun, Chief Economist for NAR, explains:

“Sales for the entire year finished strong, reaching the highest annual level since 2006. . . . With mortgage rates expected to rise in 2022, it’s likely that a portion of December buyers were intent on avoiding the inevitable rate increases.”

Demand isn’t expected to weaken this year, either. In addition, the Mortgage Finance Forecast, published last week by the Mortgage Bankers’ Association (MBA), calls for existing-home sales to reach 6.4 million homes this year.

Supply Is Very Limited

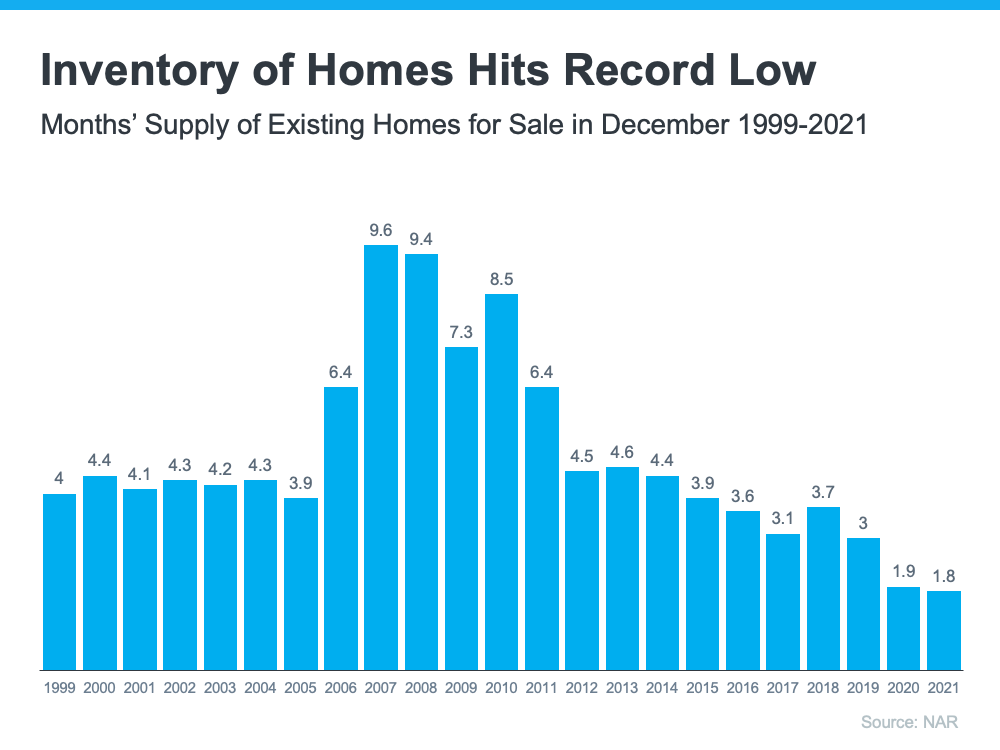

The same sales report from NAR also reveals the months’ supply of inventory just hit the lowest number of the century. It notes:

“Total housing inventory at the end of December amounted to 910,000 units, down 18% from November and down 14.2% from one year ago (1.06 million). Unsold inventory sits at a 1.8-month supply at the present sales pace, down from 2.1 months in November and from 1.9 months in December 2020.”

The reality is, inventory decreases every year in December. That’s just how the typical seasonal trend goes in real estate. However, the following graph emphasizes how this December was lower than any other December going all the way back to 1999.

Right Now, Sellers Have Maximum Leverage

As mentioned above, when there’s strong demand for an item and a limited supply of it available, the seller has maximum leverage in the negotiation. In the case of homeowners who are thinking about selling, there may never be a better time than right now. While demand is this high and inventory is this low, you’ll have leverage in all aspects of the sale of your house.

Today’s buyers know they need to be flexible negotiators that make very competitive offers, so here are a few areas that could tip in your favor when your house goes on the market:

Competitive sales price

Flexible closing date

Potential for a leaseback to allow you more time to find a home

Minimal offer contingencies

Bottom Line

If you’re thinking of selling your house this year, now is the optimal time to list it. Let’s connect to discuss how you can put your house on the market today.